Introduction

Free enterprise capitalist countries such as the USA and Great Britain have experienced rapid long-term economic growth, but this growth has not been smooth and steady. Instead, there have been periodic short-run fluctuations in output, income, employment and prices around the long-term upward trend of GNP.

Periods of high output, income and employment are called expansion, upswing or prosperity, while periods of low economic activity are termed contraction, recession or depression. These alternating phases of expansion and contraction are known as business cycles or trade cycles.

According to J.M. Keynes, a trade cycle consists of periods of good trade marked by rising prices and low unemployment, followed by periods of bad trade characterized by falling prices and high unemployment.

Business cycles are recurrent and occur periodically, though not with perfect regularity. Their duration has varied from about two years to ten or twelve years. Some cycles have been short and mild, while others have been long with large fluctuations from the growth trend. There is no fixed or definite time pattern for these cycles.

Business cycles are economically costly. During recession or depression, large-scale unemployment prevails, leading to loss of potential output and wastage of labour and capital. Many firms incur heavy losses or go bankrupt, causing widespread human suffering and decline in living standards.

Economic fluctuations create uncertainty about future income and employment, discourage long-term investment, and increase economic risk. The severe impact of the Great Depression of the early 1930s illustrates the destructive consequences of deep downturns.

Even boom periods accompanied by inflation have social costs. Inflation erodes real incomes, particularly harming the poor, distorts resource allocation by diverting resources to unproductive uses, redistributes income in favour of the rich, and may hinder long-term economic growth.

As Crowther observed, business cycles involve both the misery of unemployment and the loss of wealth due to idle labour and capital, highlighting their serious social and economic consequences.

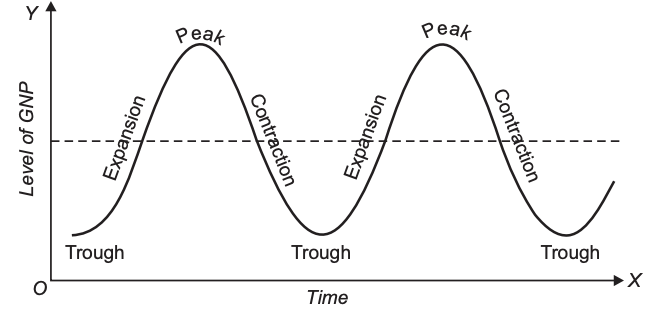

Phases of Business Cycles

- Business cycles have shown distinct phases the study of which is useful to understand their underlying causes. These phases have been called by different names by different economists. Generally, the following phases of business cycles have been distinguished :

- Expansion (Boom, Upswing or Prosperity)

- Peak (upper turning point)

- Contraction (Downswing, Recession or Depression)

- Trough (lower turning point)

A business cycle begins from the trough or depression where economic activity, output and employment are at their lowest level. With revival, the economy enters the expansion phase, but expansion cannot continue indefinitely; after reaching the peak (upper turning point), contraction or downswing begins, leading again to depression and completing the cycle. After remaining at the trough for some time, recovery starts and a new cycle begins.

According to Haberler, the four phases of a business cycle are: upswing (expansion), upper turning point (peak), downswing (contraction), and lower turning point (trough).

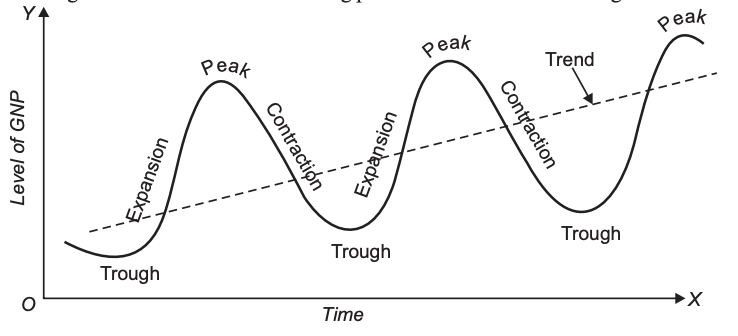

One pattern of cyclical fluctuation occurs around a stable equilibrium level, where economic activity fluctuates without any long-term growth trend. This represents dynamic stability with change but no sustained rise in output.

The second pattern shows cyclical fluctuations around a rising growth path, where economic activity follows an upward long-term trend while still experiencing periodic expansions and contractions.

J.R. Hicks explained such growth-oriented cycles by incorporating factors like autonomous investment, population growth and technological progress into the analysis, which generate long-term economic growth alongside cyclical fluctuations.

Expansion and Prosperity:

During the expansion phase of the business cycle, output and employment rise steadily until full-employment of resources is achieved and production reaches its maximum possible level given available resources. Only frictional and structural unemployment exist, and there is no involuntary unemployment.

In prosperity, the gap between potential GNP and actual GNP becomes zero, net investment is high, demand for durable consumer goods increases, and prices generally rise. Despite rising prices, high income and employment levels result in improved standards of living.

Expansion cannot continue indefinitely. It may end due to factors such as reduction in bank credit or a decline in profit expectations, leading businessmen to become pessimistic about the future.

Monetarists argue that contraction in bank credit is a major cause of the downswing, as reduced credit availability lowers investment and spending.

Keynes attributed the downturn to a sudden collapse in the marginal efficiency of capital (MEC), meaning a sharp fall in expected profitability of investment. According to him, the decline in investment triggers contraction and initiates the downswing in economic activity.