INTRODUCTION

J.R. Hicks explained business cycles through the interaction of multiplier and accelerator, constrained by a ceiling (full-employment level of output) and a floor (minimum level of economic activity), and integrated cyclical fluctuations with long-term economic growth.

Hicks’s model is a non-linear dynamic framework where output fluctuates around a rising growth trend due to multiplier–accelerator interaction subject to upper and lower bounds.

Kaldor developed another significant Keynesian non-linear model of business cycles, modifying the rigid accelerator assumption and providing a more flexible dynamic structure.

R.M. Goodwin also proposed a non-linear dynamic growth-cycle model, explaining cyclical fluctuations around a steady growth path similar to Hicks but with different structural assumptions.

Milton Friedman presented a monetarist theory of trade cycles, analyzing business fluctuations through changes in money supply and monetary disturbances rather than multiplier–accelerator interaction.

Thus, major modern theories of business cycles include Hicks’s growth-cycle model, Kaldor’s non-linear Keynesian model, Goodwin’s dynamic growth-cycle model, and Friedman’s monetarist explanation based on monetary factors.

KALDOR’S MODEL OF BUSINESS CYCLE

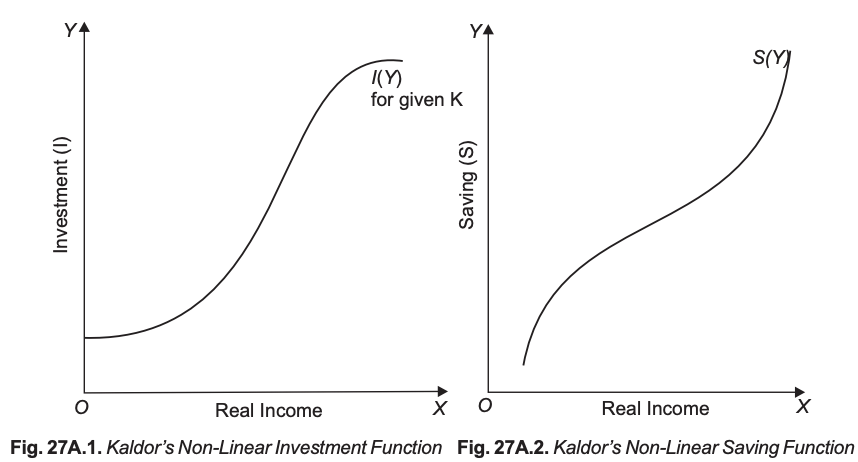

In Kaldor’s model of trade cycles, economic activity (aggregate output and employment) is determined by the interaction of specially shaped saving and investment functions.

The equilibrium level of income is obtained where saving equals investment:

$$S(Y) = I(Y)$$Both saving and investment functions are non-linear and possess peculiar shapes, unlike the simple linear forms used in basic Keynesian models.

The intersection of these saving and investment curves yields three equilibrium points: two stable equilibria and one unstable equilibrium.

The stable equilibria represent positions toward which the economy tends to move after a disturbance, while the unstable equilibrium represents a point from which the economy diverges when disturbed.

Thus, cyclical movements in income and employment arise from the non-linear interaction of saving and investment functions around these multiple equilibrium points.

Kaldor’s Investment Function

In Kaldor’s investment function, investment depends on the level of income (economic activity) and the stock of capital:

$$I = f(Y, K),$$

where \(\frac{\partial I}{\partial Y} > 0\) and \(\frac{\partial I}{\partial Y}\) represents the marginal propensity to invest.Unlike the rigid accelerator principle \(\big(I = v(Y_t – Y_{t-1})\big)\), Kaldor relates investment to the level of income rather than the rate of change of income. Thus, investment depends on aggregate output or employment itself, not merely on its growth.

Kaldor incorporates the effect of capital accumulation on productive capacity and entrepreneurial decisions; higher capital stock reduces profitable investment opportunities, making the investment function non-linear.

The non-linear investment curve shows a normal or moderate marginal propensity to invest in the middle range of income, but marginal investment propensity is low at both very low and very high levels of economic activity.

At low income levels, weak profit expectations reduce investment responsiveness; at high income levels, diminishing economies of scale and rising financial costs lower marginal propensity to invest.

Kaldor also assumes an inverse relationship between investment and capital stock:

$$\frac{\partial I}{\partial K} < 0.$$

As capital stock accumulates, productive capacity expands and investment opportunities shrink, causing the investment function to shift downward.Therefore, continuous capital accumulation reduces investment at each level of income, reinforcing the non-linear character of the investment function, which plays a central role in generating trade cycles in Kaldor’s model.