Earlier theories of business cycles include Keynes’s theory, Samuelson’s multiplier–accelerator interaction model, Hicks’s ceiling–floor model, Kaldor’s non-linear saving–investment model, and Goodwin’s growth-cycle model; these developments largely extend original Keynesian analysis with modifications.

These Keynesian and post-Keynesian models emphasize aggregate demand, multiplier–accelerator interaction, and capital accumulation as key forces behind cyclical fluctuations.

In the post-Keynesian era, Milton Friedman introduced the Monetarist Theory of Business Cycles, shifting focus to changes in money supply as the primary cause of economic fluctuations.

From the early 1980s, Robert Lucas led another macroeconomic revolution by proposing the New Classical Theory or Rational Expectations Theory of business cycles, emphasizing rational expectations, market clearing, and policy ineffectiveness.

In response, Keynesian economists developed the New Keynesian Theory of Business Cycles, incorporating rational expectations and microfoundations while retaining price and wage rigidities as explanations for output fluctuations.

Thus, modern business cycle theory evolved through three major strands: Monetarist (money supply-driven cycles), New Classical (rational expectations and market clearing), and New Keynesian (imperfect competition and nominal rigidities).

FRIEDMAN’S MONETARIST THEORY OF BUSINESS CYCLES

Friedman and Schwartz propounded the Monetarist Theory of Business Cycles, arguing that instability in growth of money supply is the principal source of cyclical fluctuations in output and employment.

They view the free market economy as inherently stable; cyclical instability arises from exogenous money shocks (changes in money supply) that affect aggregate demand and thereby economic activity.

Based on U.S. historical data, they found a strong correlation between cyclical movements in money stock and economic activity, and concluded that causation runs from changes in money supply to changes in output, not vice versa.

In contrast to Keynes, who emphasized autonomous changes in investment as the driver of fluctuations, Friedman stressed exogenous changes in money stock as the primary cause of changes in aggregate demand and national income.

Monetarists introduced the concept of money multiplier, expressing the relationship between change in money supply and change in income:

$$\frac{\Delta Y}{\Delta M},$$

where \(\Delta Y\) = change in national income and \(\Delta M\) = change in money stock.This contrasts with the Keynesian investment multiplier, which measures the relationship between change in autonomous investment and resulting change in income:

$$\frac{\Delta Y}{\Delta I}.$$Monetarists argue that the money multiplier is more stable than the Keynesian investment multiplier, which varies due to leakages such as imports and taxation.

Therefore, they claim that the relative stability of the money multiplier provides stronger support for the monetarist explanation of cyclical fluctuations driven primarily by changes in money supply.

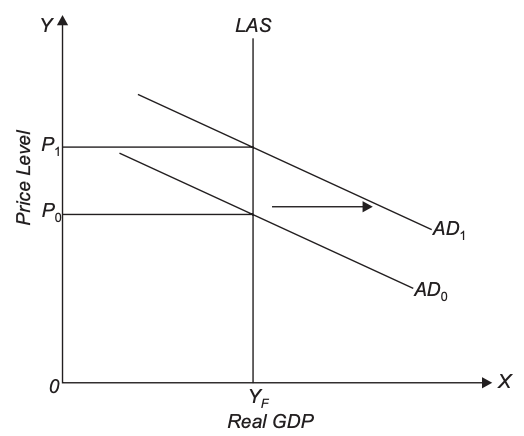

Monetarist Theory : Changes in money supply do not affect real GDP in the long run ; they affect only the price level