Government borrowing is an important fiscal instrument for mobilising community savings and financing economic development programmes, especially in developing economies.

Since taxation alone cannot generate sufficient resources for development and excessively high taxes may discourage private saving and investment, governments often resort to public borrowing to supplement development finance.

Public borrowing enables the government to raise funds for infrastructure, industrial development, and other productive investments without imposing an excessive tax burden on the economy.

When a fiscal deficit (budget deficit) arises, it can be financed through two main methods: borrowing from the market or creating new money.

Financing the deficit through government borrowing is known as debt financing, and it results in an increase in public debt as the government raises resources from individuals, institutions, and financial markets.

The second method is money financing, under which the government finances the deficit by printing new money, thereby increasing the money supply in the economy.

The extent to which money financing should be used depends on whether the newly created money is utilised for productive purposes that generate higher output, income, and economic growth.

In a developing economy, an appropriate balance must be maintained among taxation, borrowing, and money creation so that adequate resources are mobilised for development without creating excessive inflation, debt burden, or adverse effects on private investment.

Therefore, a carefully designed combination of taxation, debt financing, and money financing is essential for achieving sustainable economic growth and development.

BORROWING OR DEBT-FINANCING OF BUDGET DEFICIT

Debt financing (bond financing) of budget deficit occurs when the government borrows money by issuing bonds and selling them to the public, usually through banks and other financial intermediaries that use public deposits to purchase these bonds.

Borrowing enables the government to increase expenditure immediately, but it simultaneously increases public debt, creating both short-run and long-run economic consequences.

Budget deficit may also arise from tax reductions while government expenditure remains unchanged. Such deficits can likewise be financed through borrowing from banks or the public.

Government borrowing creates future obligations because it must pay annual interest payments and eventually repay the principal amount, which may require higher taxes in the future.

According to the Keynesian view, debt-financed government expenditure has an expansionary effect on the economy. An increase in government spending shifts aggregate expenditure (C + I + G) upward and raises national income and output.

When the economy operates below full employment and an output gap exists, debt-financed government expenditure increases production, employment, and income rather than merely raising prices.

As national income rises, tax collections automatically increase at the existing tax rates. This increase in revenue can gradually reduce the budget deficit and may even restore budget balance over time.

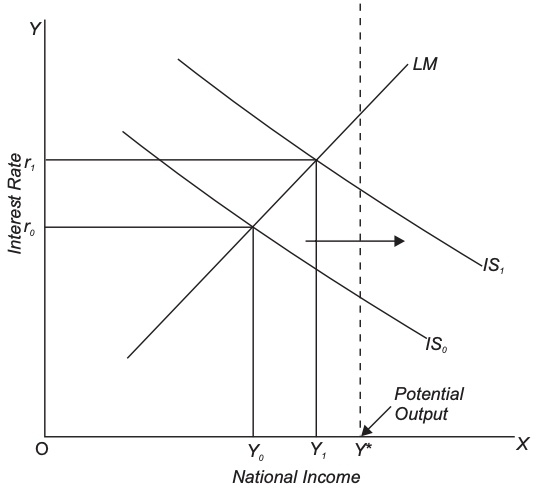

In the IS-LM framework, debt-financed government spending shifts the IS curve rightward, increasing equilibrium income from Y₀ to Y₁ while the LM curve remains unchanged.

Although interest rates rise due to higher government borrowing, the increase is not large enough to completely offset the positive impact of higher government expenditure. Therefore, there is a net expansionary effect on output and income.

Critics argue that debt-financed expenditure generates a crowding-out effect on private investment, reducing the effectiveness of fiscal expansion.

Government borrowing increases the demand for loanable funds, causing interest rates to rise. Higher interest rates make borrowing more expensive for businesses, leading to a decline in private investment.

Due to reduced private investment, critics believe that much of the expansionary impact of government spending is offset, while society still bears the burden of a larger public debt.

Even when budget deficits arise from tax cuts rather than higher government spending, crowding out may occur. Lower taxes increase disposable income and consumption expenditure, reducing private savings.

Reduced savings decrease the supply of loanable funds, pushing interest rates upward and discouraging private investment.

Thus, while Keynesians emphasize the income- and output-expanding effects of debt-financed deficits, critics stress the rise in interest rates, decline in private investment, and long-term burden of public debt.

Curves Approach