General Equilibrium: Meaning

Pareto efficiency (or economic efficiency) is better analysed through general equilibrium analysis rather than partial equilibrium analysis because achieving economic efficiency involves multiple consumers, firms, goods, and factors simultaneously.

In general equilibrium analysis, the prices and quantities of all goods and factors are treated as variables, and their equilibrium is determined simultaneously across all product and factor markets.

The economy consists of extensive interrelationships and interdependence among commodity and factor markets, along with numerous decision-making agents such as consumers, producers, workers (suppliers of labour), and other resource owners.

These economic agents are assumed to be self-interested and seek to maximise their respective objectives:

Consumers maximise utility.

Producers maximise profits.

A comprehensive understanding of the economy, taking account of all market interdependencies and interactions among agents, can only be achieved through general equilibrium analysis.

General equilibrium exists when:

All commodity markets are simultaneously in equilibrium.

All factor markets are simultaneously in equilibrium.

All decision-making agents—consumers, producers, and resource owners—are simultaneously in equilibrium.

General equilibrium analysis therefore explains the simultaneous equilibrium of all markets when the prices and quantities of all goods and factors are treated as variables.

The conditions for Pareto efficiency are commonly explained using a simplified general equilibrium framework consisting of:

Two individuals.

Two goods.

Two factors of production.

The Edgeworth Box Diagram as the analytical tool.

Before analysing Pareto efficiency, the Edgeworth Box Diagram is used to explain general equilibrium in a pure exchange economy.

In a pure exchange economy, there is no production; the available quantities of goods are assumed to be provided from outside the system.

To simplify analysis, the pure exchange model assumes:

Two goods, available in fixed quantities for consumption.

Two individuals, between whom exchange of these goods takes place.

The objective of exchange is to achieve equilibrium in the distribution of the given quantities of the two goods between the two individuals.

Edgeworth Box and General Equilibrium of Exchange

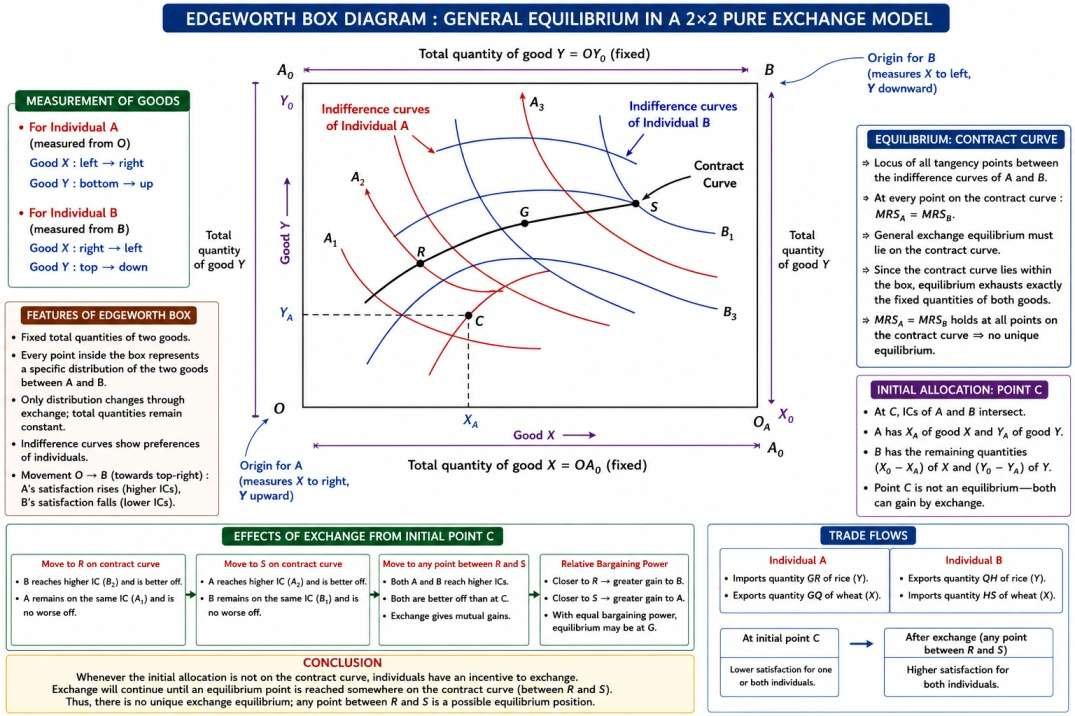

In a two-goods, two-individuals (2×2) pure exchange model, the Edgeworth Box Diagram is used to explain the general equilibrium distribution of two goods between two individuals.

The Edgeworth Box has fixed dimensions determined by the total available quantities of the two goods:

Total quantity of good X = OA₀.

Total quantity of good Y = OY₀.

Since the total quantities are fixed, the dimensions of the box are fixed.

For individual A, quantities of X and Y are measured from the bottom-left origin (OA):

Good X is measured from left to right.

Good Y is measured from bottom upwards.

For individual B, quantities are measured from the top-right origin (OB):

Good X is measured from right to left.

Good Y is measured from top to bottom.

The Edgeworth Box represents the complete distribution of the fixed quantities of the two goods between the two individuals, and it is assumed that the entire available quantities of both goods are consumed by them.

Every point inside the Edgeworth Box represents a specific distribution of the two goods between the two consumers.

When individuals exchange goods:

They move from one point in the box to another.

Quantities bought and sold of each good are equal.

Only the distribution of goods changes.

The total quantities of both goods remain constant.

The Edgeworth Box contains the indifference curves of both individuals representing their preferences between the two goods.

As movement occurs from the bottom-left corner toward the top-right corner:

Individual A reaches successively higher indifference curves and gains satisfaction.

Individual B reaches successively lower indifference curves and loses satisfaction.

The general exchange equilibrium lies on the contract curve, which is the locus of all tangency points between the indifference curves of the two individuals.

At every point on the contract curve:

The Marginal Rate of Substitution (MRS) of individual A equals the MRS of individual B.

General exchange equilibrium requires:

MRSA = MRSB.

Since every point on the contract curve lies within the Edgeworth Box, equilibrium distribution exhausts exactly the fixed available quantities of both goods.

The condition MRSA = MRSB alone does not determine a unique equilibrium point because it is satisfied at all points on the contract curve.

To identify the possible equilibrium range, the initial distribution of goods between the individuals must be known.

If the initial allocation is represented by point C:

Individual A possesses quantities XA and YA.

Individual B receives the remaining quantities of both goods.

At point C, the indifference curves of the two individuals intersect.

The initial distribution at point C cannot be an equilibrium position because both individuals can improve their welfare through exchange and move toward the contract curve.

As long as both individuals expect gains from exchange, they will continue trading until they reach some point on the contract curve.

If exchange moves the economy from point C to point R on the contract curve:

Individual B reaches a higher indifference curve and becomes better off.

Individual A remains on the same indifference curve and is no worse off.

If exchange moves the economy from point C to point S:

Individual A becomes better off.

Individual B remains no worse off than at point C.

If exchange leads to any point between R and S on the contract curve:

Both individuals become better off relative to the initial allocation.

Exchange generates mutual gains.

The closer the equilibrium lies to R, the greater is the gain of individual B; the closer it lies to S, the greater is the gain of individual A.

The exact equilibrium position on the contract curve depends on the relative bargaining power of the two individuals.

If bargaining power is approximately equal, equilibrium may occur at a point such as G, where both individuals gain nearly equally from exchange.

Whenever the initial allocation is not on the contract curve, individuals have an incentive to exchange goods because moving toward the contract curve increases their satisfaction.

Exchange equilibrium can exist at any point between R and S on the contract curve; therefore, although equilibrium must lie on the contract curve, there is no unique exchange equilibrium, and all points between R and S are possible equilibrium positions.