Introduction

Short-run fluctuations in aggregate demand can cause deviations of output and employment from potential GDP, but classical and New Classical economists argue that wage and price flexibility ensures such demand changes affect only nominal variables, leaving real output and employment unchanged.

In contrast, Keynes and earlier Keynesians assumed wage and price stickiness, meaning that in the short run wages and prices do not adjust quickly, so changes in aggregate demand primarily influence output and employment rather than prices.

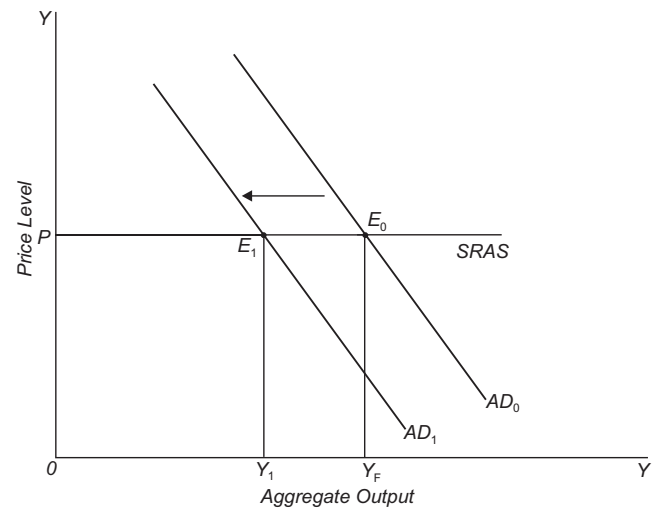

In the traditional Keynesian model, the short-run aggregate supply curve (SRAS) is horizontal, implying fixed price levels; thus, a leftward shift in aggregate demand (due to reduced investment or money supply) lowers equilibrium output and leads to recession.

New Classical economists criticise this assumption of price rigidity as lacking solid microeconomic foundations, since it conflicts with rational, profit-maximising behaviour.

To address this weakness, New Keynesian Economics provides microeconomic explanations for short-run price stickiness, strengthening the theoretical basis of Keynesian analysis while retaining its core insight about short-run non-adjustment.

Unlike the traditional Keynesian model, New Keynesian models assume imperfect competition rather than perfect competition; firms face downward-sloping demand curves, meaning price cuts may not significantly increase sales if rivals also adjust prices.

Because firms behave optimally and rationally under imperfect competition, they may choose not to change prices frequently, providing a micro-founded explanation for price stickiness and short-run fluctuations in output and employment.